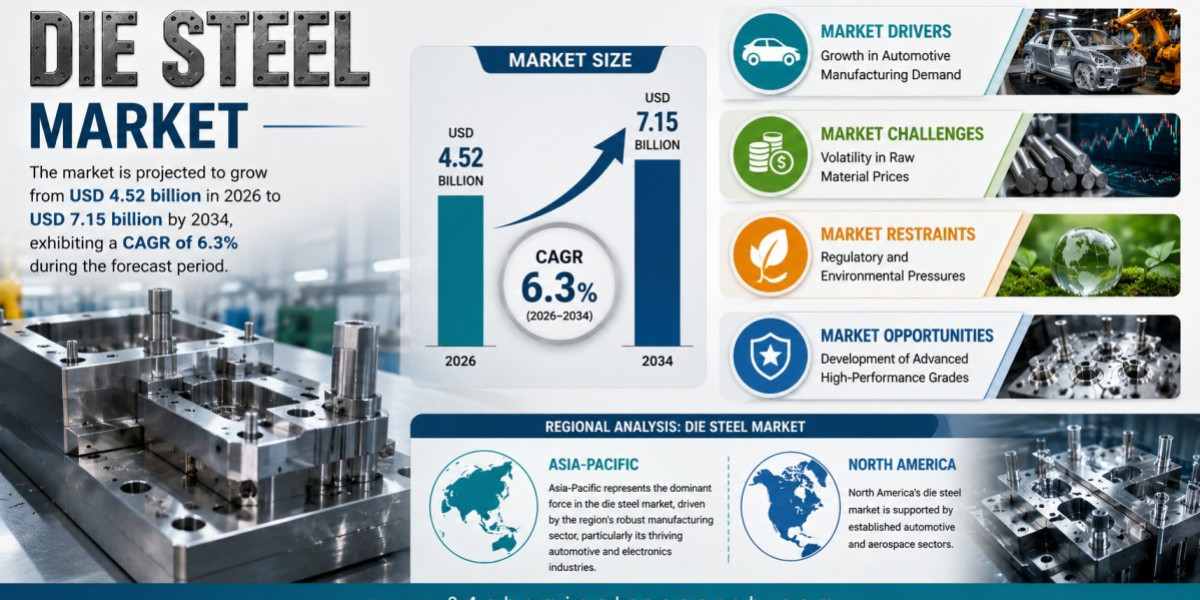

Global die steel market size was valued at USD 4.23 billion in 2025. The market is projected to grow from USD 4.52 billion in 2026 to USD 7.15 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Die steel refers to high-strength, wear-resistant alloy steels specifically engineered for the production of dies used in metal forming, stamping, extrusion, and forging processes. These specialized steels are designed to withstand extreme mechanical stresses, thermal cycling, and abrasive wear, ensuring prolonged tool life and dimensional accuracy. The market growth is driven by rising demand from the automotive industry, which accounts for approximately 45% of global consumption, the expansion of aerospace and defense sectors, and increasing requirements for lightweight materials in manufacturing.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310715/die-steel-market

Market Overview & Regional Analysis

Asia-Pacific represents the dominant force in the die steel market, driven by the region's robust manufacturing sector, particularly its thriving automotive and electronics industries. China, Japan, and South Korea are key contributors to this demand, with substantial investments in advanced manufacturing technologies. The region's focus on precision engineering and automotive production further solidifies its position as the leading consumer of die steel. The availability of skilled labor and well-established supply chains also contribute to market growth, with a growing emphasis on developing new alloy compositions to meet the evolving needs of the automotive and aerospace industries.

North America exhibits a steady demand for die steel, primarily supported by the automotive and aerospace sectors. The region's commitment to advanced manufacturing and technological innovation drives the need for high-quality die steels. While the market is relatively mature, ongoing investments in electric vehicle production are creating new opportunities. The focus on lightweighting and improved fuel efficiency translates to demand for specialized die steel alloys. The presence of strong research and development capabilities and established supply chains contribute to the region’s maintained market share.

Key Market Drivers and Opportunities

The automotive industry remains the largest consumer of die steel, accounting for 45% of global demand. As passenger vehicle production continues to rise, particularly in emerging economies like China, India, and Mexico, automakers require high-performance tool steels for stamping dies, forging dies, and extrusion tools. The shift toward lightweight materials such as advanced high-strength steel (AHSS) and aluminum further amplifies demand, as these materials necessitate harder, more wear-resistant dies. The surge in electric vehicle (EV) production introduces new requirements for specialized die steels capable of handling complex battery tray and structural component manufacturing.

Innovation in alloy design presents a significant opportunity for die steel manufacturers to capture premium markets in high-precision industries. The development of ultra-clean, vacuum-remelted die steels with enhanced toughness and thermal stability addresses growing demands from automotive hot stamping and aerospace forging. For example, steels with 10% chromium and nitrogen alloying have demonstrated a 30% increase in die life in hot-work applications. Additionally, the medical device sector is emerging as a high-growth niche, with demand for precision-engineered dies expected to grow at a compound annual rate of 6.2% as global medical device market revenues are projected to reach USD 718 billion by 2027.

Challenges & Restraints

The die steel market is highly sensitive to fluctuations in the prices of key alloying elements such as nickel, chromium, vanadium, and tungsten, which account for up to 60% of raw material costs. Small and medium-sized manufacturers, which lack long-term supply contracts, face particularly acute margin pressures. The industry also faces increasing regulatory scrutiny over carbon emissions, energy consumption, and waste management. Production of high-alloy die steels typically involves energy-intensive processes contributing approximately 1.8 tons of CO₂ per ton of steel produced. Stringent environmental regulations, particularly in the European Union under the Carbon Border Adjustment Mechanism (CBAM), impose additional compliance costs and carbon taxes.

Market Segmentation by Type

Cold-work steel

Hot-work steel

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/310715/die-steel-market

Market Segmentation by Application

Stamping

Forging

Extrusion

Others

Market Segmentation and Key Players

Kennametal (United States)

Sandvik Materials Technology (Sweden)

Mitsubishi Materials (Japan)

ISCAR (Israel)

Thyssenkrupp Materials (Germany)

Sumitomo Electric Industries (Japan)

VDM Metals (Germany)

JFE Steel (Japan)

Dursteel (India)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Die Steel, covering the period from 2026 to 2034. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on sales, sales volume, and revenue forecasts, as well as detailed segmentation by type and application.

In addition, the report offers in-depth profiles of key industry players, including company profiles, product specifications, production capacity and sales, revenue, pricing, gross margins, and sales performance. It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth. As part of this research, we surveyed die steel manufacturers, suppliers, distributors, and industry experts. The survey covered revenue and demand trends, product types and recent developments, strategic plans and market drivers, as well as industry challenges, obstacles, and potential risks.

Get Full Report Here: https://www.24chemicalresearch.com/reports/310715/die-steel-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/